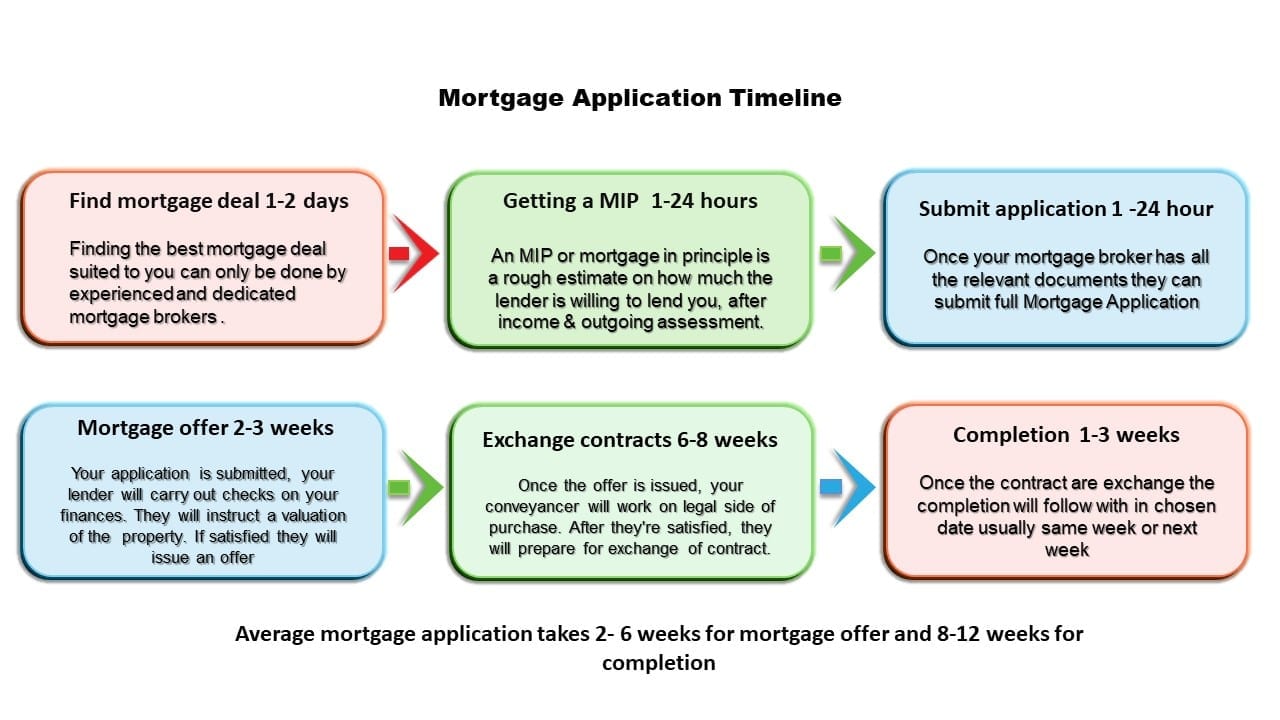

Mortgage Application Timeline

| Free Mortgage Broker | |||

| TRUSTED MORTGAGE BROKER | |||

|

How Long Does A Mortgage Application Take To Offer?

Normally 2 to 4 Week from mortgage application to offer.

Once you have found your desired home you must be ready to submit your mortgage application. But starting a mortgage can be a daunting task. Many home-movers and first-time buyers alike have a variety of questions, and the answers may not be that clear. At Marianna FS, we have released this mortgage guide, alongside countless others, in order to help you with your mortgage journey.

In this article we’ll cover:

- The Mortgage application timeline.

- Documents required for a mortgage application.

- How long does it take to get a mortgage offer?

- What can you do to speed up your mortgage application?

- What factors can delay a mortgage application?

The Mortgage Application Timeline.

Actually completing your mortgage application will only take a day or so, sometimes even less. Your mortgage application can take from 2 to 6 weeks to be approved and issue a mortgage offer.

You will need to make sure all your finances and financial info are prepared beforehand, in order to speed up the case. Lenders will want proof of your reliability, credit worthiness, proof of income, and more. To do these checks they will need to access the following:

- Details of your outgoings/expenses, including loans and credit cards you may have.

- Proof of your total earned income.

- A form of ID in order to prove your identity and proof of address.

The mortgage application process involves the following stages.

1. Finding the best mortgage deal – 1 to 2 days.

Mortgage payments are the biggest expense for a borrower. This means that finding the best mortgage deal is the upmost priority in your mortgage application. If you’re looking for the best first time buyer mortgages rates or for the best remortgage deals, working with a no fee mortgage broker can save you big money on broker fees while still securing the best mortgage deal available to you.

An Application through a mortgage broker can be a lot quicker than going directly to the bank. Some people choose to compare rates online and do the application themselves, but that can be confusing and time consuming. Instead, working with a fee free mortgage broker can save you time, money and seed up your mortgage application approval time.

2. Getting a Mortgage in Principle – 1hour to 1day.

Before even applying for a mortgage, you will need to know how much you can borrow. A Mortgage in principle (MIP) tells you just this, giving you a reasonable idea of what is your budget .

Based on the information provided, your mortgage broker will complete the fact-find form while gathering all the necessary info about your income and outgoing. Once this form is completed and sent to your bank, you can get your decision in principle, which can be obtained as quick as 1 to 24 hours.

A Mortgage in principle does not guarantee mortgage approval.

3. Submitting your mortgage application – 30 minutes to 1hour.

Once your property purchase offer is accepted then the next step is to submit a mortgage application. If you are wondering how long mortgage application take then this can be a lot quicker if you use mortgage broker to submit your application.

Your mortgage broker will collect all the relevant supporting documents for the mortgage application like Bank statements, income proof like payslips or SA302, a tax overview and deposit proof. Having all the documents handy can save you a lot of time in the mortgage approval process.

4. Getting a mortgage offer – 2 to 4 weeks from application

Once the mortgage application is submitted your lender will carry out all necessary checks on your income and outgoings. Then the lender will instruct a valuation of the property you wish to purchase. After a successful valuation and income assessment, your lender will issue a mortgage offer.

From the mortgage application to a mortgage offer, it takes roughly 2-4 weeks in general. This can vary from bank to bank, depending on the type of the property, loan to value and the applicant’s financial circumstances.

5. Exchange of contracts and completion

Once the mortgage offer is issued, your Conveyancer will continue to work on the legal side of things, like raising an enquiry. After the Conveyancer is satisfied, they will prepare for the exchange of contracts and completion, which can take around 3 – 6 weeks after the mortgage offer.

Once the exchange and completion date is set, the conveyancer will request the deposit from the buyer and request the remaining funds from The lender can take up to 3-6 days to release the funds necessary.

On the day of completion your conveyancer will transfer the money to the seller, conveyancer and you have completed the purchase.

How long does it take to get a mortgage offer after valuation?

After submitting the application, your Bank/lender will review and assess the submitted info, They will then arrange a survey on the property you’re buying, to make sure it meets safety requirements and is actually worth the amount of money they’re lending.

This can take up to 3 days to 1 week, depending on the property.

The surveyor will report back to the lender after their assessment. The Case worker or an underwriter will then review and validate the valuation. If all the information is satisfactory then the mortgage offer is typically issued within 1 to 2 weeks, depending on the survey.

Always remember the survey is carried out by the lender as it is only for their benefit to check the property is worth the purchase price. As a homebuyer you can also arrange your own survey to check the condition of the property for your own safety.

What documents are required for a Mortgage Application?

The documents required for your mortgage application generally include:

- 3 months worth of pay slips with P60 if employed.

- SA302 and Tax Overview for 2 years if you are self employed.

- 3 months of bank statements.

- Proof of ID’s for all applicants.

- Proof of address for all applicants.

- Bank statements to show the deposit.

These are the basic documents needed to complete a mortgage application. Your lender may need more information depending on the case and the property.

Why does my mortgage application take so long?

There are many factors that can delay a mortgage application, some include:

- Not being prepared with documents such as bank statements, proof of income, ID, and others, which often delays the mortgage application.

- Having an especially complex case /complex income types or can be the property types can be caused to delay the mortgage application.

- During busy periods lenders take a lot longer to do financial assessment which can delay the process.

- Not having a Mortgage Broker on your case can severely restrict the pace of your mortgage application, as this means you don’t have a dedicated professional on your case.

In order to avoid these hiccups in your application, it is advisable to have all necessary documentation, such as the ones listed, to hand. This means there are no delays where the bank doesn’t have enough info to continue with your case.

Working with an experienced broker can help you speed up the process, as they are trained professionals who can ensure a hi quality and fast mortgage approval.

Can a mortgage broker speed up the mortgage application process?

The last bullet point on the previous list is perhaps the most important of them all. The right Mortgage brokers are probably the most important factor in your mortgage application

Many believe that the fees mortgages brokers charge are way too high, in some cases rising to 1% of the loan amount! This, however, doesn’t apply to all brokers, as Fee-Free mortgage firms like Marianna FS are ready and willing to assist you on your mortgage journey, all for free! Visit Marianna FS to see for yourself.

In a nutshell, the minimum time needed to get a mortgage application approval is around 1-2 weeks, subject to circumstances though this can be very difficult without a Mortgage broker, who can save you time, effort and money in getting your mortgage approval done a lot quicker.

How long does a mortgage offer last?

Typically, mortgage offers last for six months before expiring, but the purchase transaction can take longer. A remortgage offer can be valid for only 3 months as a remortgage is a quicker process. But in this day, mortgage lenders typically issue mortgage offers with six months of validity which can be extended for 30 days with a valid reason.

What factors can delay a Mortgage application approval time?

Having a complex or inconsistent income can increase the underwriting timing, resulting in possibly failing affordability checks. A problem with the valuation of the property may also result in a delay of the mortgage application. Sometimes, changing your name can cause a delay. Bad credit can be a more certain factor that can delay the mortgage application approval time.

Should I use a mortgage broker or go direct to bank for mortgage application?

Simply put, Mortgage brokers are not restricted to one bank. This means they will handpick deals from across the mortgage market, instead of only looking at a single bank’s rates, like lenders do.

Mortgage Brokers can also complete the Mortgage in a significantly faster time compared to high street bank, as they can act as your dedicated professional. If you want to save time, effort and money it is always advisable to work with fee mortgage broker.

In summary, the time taken to complete a mortgage application can vary on many factors. But working with the right mortgage broker can be very helpful in a variety of ways.

Mortgage Application Stages

Application Preparation Stage

Before you begin the mortgage application, the pre-application stage is very important. This stage involves researching from whole of market lenders, understanding clients’ financial situations regarding their needs, and collecting the necessary documents. Evaluating credit scores and income assessment are essential to determine eligibility for a mortgage.

Mortgage Application Submit

The mortgage application stage is where you formally apply for the mortgage. You will need to complete the lender’s application form and submit required documents, such as proof of income, property details, and identification. Having correct documents can prevent delays in mortgage application process. During this stage, the lender will assess your mortgage application. Mortgage application timeline can change on the what type documents provided at the application.

Mortgage Application Processing or Underwriting

Once mortgage application is submitted then lender will begins underwriting the mortgage application. During this stage, the lender will verify applicant information like name, address and carry out valuation of the property you intend to buy on mortgage. The valuation is a important part of the mortgage application process as it determines if property is worth the price.

The underwriting phase is one of the most critical steps in the mortgage application. In this phase, the lender’s underwriter evaluates your entire financial profile to determine the risk of lending to you. On many occasions underwriter may request additional information or clarification on certain aspects of your application.

Mortgage approval in the underwriting means you are one step closer to obtaining your mortgage against property you want to buy.

Mortgage Offer

Once the underwriting is successfully completed, and if they are happy with the assessment then lender will issue a formal mortgage offer. The mortgage offer copy is sent to solicitors and applicants. Mortgage offer outlining the loan amount, interest rate, and terms.

Legal Work and Completion

By the time mortgage offer been approved your solicitors will begin the legal work on the property purchase. Conveyancing on the property purchase is the longest part in mortgage application timeline. This involves checking all the legal information about the property like land registry and raising enquiries. After completing the legal work buyer solicitors and seller solicitors decide the completion date suitable to all the parties.

Related guides

How Long It Takes To Remortgage

How Much A Mortgage Broker Charge.

What Documents Required To Remortgage?

Mortgage Application Time Through A Mortgage Broker.